One of the most important decisions a business (c-suite/board/leadership team/investors) can make is which flavour of innovation is the right fit for their ambition in relation to countering disruption, creating compelling customer product experiences, moving from an analog to a cognitive business and also embracing new business models.

There are 7 core flavours of innovation, which need to be assessed against the culture, funding model, operating model and risk profile of your business, as not all flavours combine well within traditional organisations.

It is critical that you define what ‘innovation’ means and stands for within your organisation and these flavours can assist you in this task. In a post-COVID19 world, there will need to be a balance struck between how businesses maintain their core business models, but it will be those that are able to thread innovation deeper into the DNA of their people, processes, platforms and products who will survive and thrive.

So, here are the core 7 flavours, and the question to ask yourself as you read this post is:

“Which flavour is the right fit for our ambition, culture and risk appetite right now, but will also allow these 3 areas to change into the future?”

1. Disruptive Innovation: Clayton Christensen

In 1995 Clayton Christensen introduced the concept of disruptive innovation (alongside sustaining innovation) which has become one of the foundational theories of the technology & startup industry, with everyone from Steve Jobs to Reed Hastings to Jeff Bezos citing it as an influence.

Christensen wanted to explain how small companies — with few people and highly limited resources — could, in certain circumstances, unseat much larger and better-capitalized incumbents using technology and understanding signals better than the incumbents.

He argued that as companies get larger and ‘fatter’, they shift focus from acquiring new customers to retaining their most valuable ones. This strategy — meant to create stability and maintain maximum revenue — inevitably leads to some swath of that company’s potential customers being overlooked.

Startups get a foothold in a market by targeting those overlooked customers and building for them. For example, startups that offer a similar service at a lower price eat away the bottom of the incumbent’s market.

If they can then start to expand upmarket while maintaining that competitive advantage, they acquire more and more of those customers. Once this happens in massive numbers, you have disruption of either the incumbent or an industry.

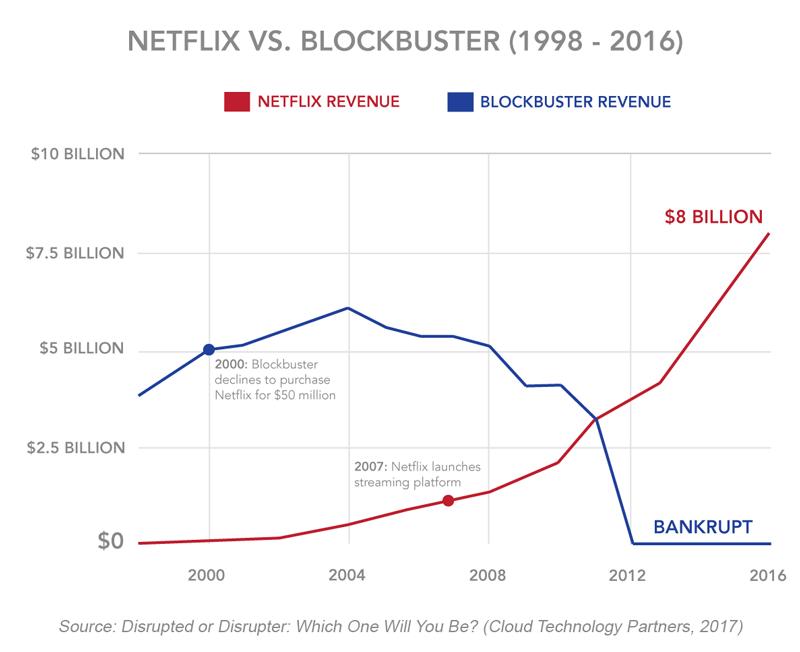

Large telcos were undercut by smaller, more nimble mobile-only services. Disk manufacturers were disrupted by competitors selling smaller disk drives. And Blockbuster was brought down by Netflix, once a modest mail-order DVD service that became an online streaming giant.

How Netflix beat Blockbuster

Blockbuster was a video rental chain that stocked the latest movie releases and had stores worldwide, peaking at 9,000 locations in 2004 (not all that long ago). However, a big portion of its revenues came from its infamous late-return fees rather than from the rentals themselves. These fees earned the company $800M in 2000 (about 16% of its revenue), according to the Associated Press, but also drove significant amounts of customer dissatisfaction.

Netflix, on the other hand, shipped DVDs ordered from its website, offering its customers unlimited rentals for a monthly subscription — with no late fee. Netflix founder Reed Hastings, aware of the antipathy many people felt towards Blockbuster’s late fees, even wove them into the origin story of the company itself, claiming for years that he started Netflix because he’d owed $40 in late fees after renting the movie “Apollo 13.”

It wasn’t just a lack of late fees that made Netflix compelling to some customers. Without the physical constraints of shelf space, Netflix could offer a vastly larger catalogue of films, including niche genres. Customers could watch movies at their own pace, didn’t have to travel to a physical store, and could mail them back when it was convenient for them.

Because Blockbuster stayed focused on new releases, the company didn’t regard Netflix as a core threat — Blockbuster even turned down the opportunity to acquire the company for $50M in 2000.

Seven years later, Netflix parlayed its direct relationship with its customers into an online streaming service. Suddenly, the monthly fee that Netflix customers paid gave them access to unlimited content, without even having to wait for a new movie to arrive in the mail. Now, it wasn’t between driving to Blockbuster and renting “The Office” or waiting for Netflix to mail a disc to you — it was between driving to Blockbuster and renting a disc or simply clicking a button on your computer screen.

While Blockbuster tried launching its own digital download service, the effort ultimately failed and the company filed for bankruptcy a few years later.

Takeaways

Today, Netflix is at the other end of the innovator’s dilemma — as one of the big incumbents in the global video streaming market, which could be worth almost $150B in the coming years, according to CB Insights’ Industry Analyst Consensus market sizing tool.

The high cost of stocking new releases contributed to Blockbuster’s downfall. Netflix is facing a similar problem today, paying more than ever to stock high-demand, licensed content as competitors like Disney, Apple, NBCUniversal, and Warner Media (HBO) enter the picture.

Netflix’s business largely depends on the content of these new competitors. Three out of the four most-streamed shows in late 2018 are owned by legacy media companies launching their own services — “The Office” (NBCUniversal), “Friends” (Warner), and “Grey’s Anatomy” (Disney). Netflix reportedly paid $100M to keep offering “Friends” for 2019, over 3x as much as it had paid in previous years. With licensed content taking up around two-thirds of total viewing hours on the platform, the question is around what will happen to Netflix if it loses these shows.

Netflix’s response to this potentially existential threat has been to increase spending on producing its own shows. It spent an estimated $15B on original content last year, according to Fast Company. But the strategy hasn’t been completely effective. In its Q2’19 investor letter, the company acknowledged that “[the quarter’s] content slate drove less growth in paid net adds than we anticipated.”

With a shrinking catalogue and increasing prices — US subscribers pay $4 per month more today than in 2014 — Netflix’s situation today is a reminder that disruption is cyclical in nature. Eventually, the disruptor becomes the incumbent, facing the threat of disruption by nimbler startups. That is why leaders in Silicon Valley are so keen to disrupt themselves before they are disrupted.

“If we don’t create the thing that kills Facebook, someone else will,” Facebook’s famous pamphlet designed to teach new hires about the company’s values notes on its last page. “It’s always Day One,” Amazon CEO Jeff Bezos regularly reminds his team and the company’s investors.

All of these are exhortations to remain aware of the possibility of disruption, as it can be extremely difficult (especially given how fast technology can evolve) to actually identify disruption when it’s happening.

2. Product Innovation: Ben Thompson

Ben Thompson, Stratechery founder and tech analyst, states that innovation comes in the form of seamless, integrated, end-to-end products that transform the user experience.

Ford invented the automobile instead of a smoother horse-drawn carriage, Sony created the Walkman instead of a refined record player, and Apple invented the iPhone instead of a nicer flip phone: all 3 are examples of product innovations that went far beyond just iterative improvements on what came before.

Many great companies create products customers didn’t know they wanted. Steve Jobs once said that Apple doesn’t do market research or hire consultants: it goes out and creates something that no one has talked about but everyone instinctively wants.

Apple does this through a deep knowledge of technology and customers, the discipline to push boundaries, and the value it places on the immeasurable experience of actually using a product.

How the iPod came to define the MP3 player category

While many think of the iPod as a revolutionary piece of technology, it was a late-comer to the MP3 player market. The first dedicated MP3 device was introduced in 1997, four years prior to the iPod’s launch. Countless manufacturers had jumped into the fray, each producing something a bit different in an attempt to nail that elusive product-market fit.

But these early MP3 players were riddled with problems. For example, because flash memory was so expensive — in 2000, 1GB of flash storage could cost over $3000 — manufacturers had to resort to bulky hard-drives. The 6GB Creative Nomad Jukebox was a behemoth, although at $500, a relatively affordable one. The portable i2Go EGo cost $2000.

In 2001, when Apple released the first generation iPod with 5GB of storage and a compact chassis at $400, it got the two most important ingredients right — size and price.

What made the iPod so appealing to consumers, however, was the experience of using it.

Other MP3 players were difficult to use. They were cluttered with buttons, often had a confusing user interface, and transferring music was a manual process. Some copyright laws of the time meant that users of products like Sony’s MC-P10 had to encode audio files in certain formats to play music.

The iPod’s click wheel and 1.5-inch screen, however, made it so that you could start using it without flipping through a manual. iTunes made transferring music and purchasing tracks more straightforward. There wasn’t a slew of hidden hurdles to jump over — you plugged it in and let the software do the work.

Apple put this “feeling” of using the iPod front and centre of its marketing. Its iconic ads featuring dancing silhouettes were upbeat and exciting. The tagline read “1000 songs in your pocket.” Instead of showcasing features and specs, the ads focused on what it feels like to listen to music on an iPod — making it seem fun and easy.

The iPod would go on to hold around a 75% market share from 2003 to 2010, an improbable and impressive feat in consumer electronics.

It would also serve as a turning point for Apple. The Atlantic’s Megan Garber writes, “[the iPod] was a launch that would lead the company, six years later, to drop ‘Computer’ from ‘Apple Computer.’”

Takeaways

Apple continues to refine and pursue its strategy to create highly integrated products with superior user experience.

The iPhone 5S, for instance, lacked in many technical aspects like clock speeds or camera resolution compared to some competitors. However, it exceeded expectations in its touch screen, battery life, and crucially, Touch ID — a technology that made it easier for people to pick up their phone and use it.

AirPods are another example. While they weren’t the first completely wireless earbuds, they soon became the most popular. Every engineering decision was made to enhance the ease and usability of the product: the charging case to make the AirPods lighter and more comfortable, the W1 chip to make Bluetooth pairing simpler, and inbuilt sensors to automatically pause music when the AirPods were taken out.

Apple invests in technology that strengthens the bond between the product and the user. That is one way the company looks to distinguish itself from rivals like Dell, Microsoft, and Samsung.

While Apple has had its product misses, they’ve mostly been products that were launched in response to market demand — such as the Newton in response to IBM’s PDA or the HomePod in response to Amazon’s Echo — rather than products that sought to redefine the market.

The next stage of product innovation is Customer Experience Innovation (see below).

3. Business Model Innovation: Fred Wilson

According to Union Square Ventures’ Fred Wilson, the most disruptive force in business isn’t new technology — it’s the business model innovation that technology enables.

In the past, many important companies were built on new technology. AT&T was built on the telephone. General Motors was built on the internal-combustion engine. Intel was built on the computer chip. Once they had the technology, the business model naturally followed: sell the product at a healthy margin.

These days, however, companies can’t rely solely on a piece of technology that they can safeguard in their vaults.

Many tech companies are turning to creative new ways to deliver products and manage costs to build a lasting business. Google did that by coming up with paid search, Facebook with ad technology, and Salesforce with a cloud-based subscription service.

How Salesforce changed the way software is sold

Salesforce upended the on-premise software model with a cloud-based subscription model, initiating one of the most important business model innovations in recent history.

In the late 90s, Oracle and SAP were dominant in the customer relationship management (CRM) market. Their complex, feature-rich products were expensive, with high fees for installation, on-site maintenance, and routine upgrades.

Marc Benioff, Salesforce’s founder, got the idea to get rid of the per-license software business model and sell access to software through the cloud. Instead of a big up-front payment and recurring payments down the line, customers could just pay a flat monthly fee — the same way they would pay a utility bill.

This eliminated the initial high-cost barrier and made the software more customizable according to the organisation’s size. Whereas Oracle and SAP had been prohibitively expensive, small companies could afford Salesforce’s scaled pricing. For large companies, Salesforce helped ease the bureaucratic headache of getting sign-off each time it became necessary to update.

Oracle and SAP couldn’t adapt quickly enough to this radical shift in selling and up-keeping software. As of 2018, Salesforce reportedly had an almost 20% market share of the global CRM market by revenue, more than double that of SAP and triple that of Oracle. And today, the business model innovation ushered in by Salesforce is conventional wisdom, with the entire software-as-a-service industry in some part owing its ubiquity to Benioff.

Takeaways

The move from desktop to cloud computing was a wide-scale business model innovation that created thousands of new SaaS companies.

For incumbents, competing with this new model meant overhauling how they’d done sales and marketing for years. For their startup competitors, it was a huge opportunity.

Many of the most exciting companies today are also eschewing technical innovation in favour of business model innovations.

In real estate, Opendoor is looking to change the traditional home-buying model. In the housing market, sellers and buyers have to act synchronously — a home seller is matched with a buyer who can make only one offer at a time.

But Opendoor wants to make transactions asynchronous — it acts as a buyer for every home that enters the market, and as a seller with a portfolio of listings for every buyer looking for a new home.

Like traditional realtors, Opendoor relies on fees to make money. But it also takes on inventory risk by buying homes directly from sellers. For buyers and sellers, the aim is to make the home-buying process easier — not as stressful and drawn-out as it’s been before.

If Opendoor can scale successfully and turn a profit, then its business model could transform the real estate world.

This is the innovation flavour which most large businesses should be focused on, as this is the most disruptive when combined with 1 & 2 on this list.

Alex Osterwalder and the Strategyzer team created the Business Model and Value Proposition Canvas work to allow businesses to counter and embrace this innovation flavour. This focuses on the fundamental disruption of a business model and the creation of new business models, which move whole industries forwards and those who are not spotting the signals, out of business.

Business model innovation doesn’t have to follow a tectonic shift in technology. It can happen in any industry where the traditional model has become inefficient or is leaving potential customers out.

4. Breakthrough Innovation: Peter Thiel

For PayPal co-founder and prolific investor Peter Thiel, just because a company invents something new doesn’t mean it is innovating.

He distinguishes what he calls “horizontal” innovation, or going from “1 to n,” from “vertical” innovation, or going from “0 to 1.”

A “0 to 1” invention is the kind of breakthrough innovation that creates companies like Google, Amazon, and Uber, when a new product comes into the world that radically changes the way an industry works. These “0 to 1” inventions don’t just become popular — in many cases, entire new industries rise up around them.

When you go from “1 to n,” on the other hand, you’re tweaking a product that already exists and creating a slightly improved or cheaper version of it. You’re copying what you already know works and applying it elsewhere.

What makes for real, “vertical” innovation, going by Thiel’s conception of it, is never going to look like something that came before. It will likely be something idiosyncratic and driven by the passion of the team behind it, whether that’s an online marketplace, a new kind of search engine, or an app on your phone that lets you summon a car at the touch of a button.

How Uber went from 0 to 1

Uber built one of the fastest-growing tech startups of all time by bringing a well-timed vertical “0 to 1” innovation into the world of transportation.

When Uber launched, the iPhone was on its third iteration — still in the early phases of world domination. But the iPhone had something incredibly powerful that Uber leveraged: GPS. Thousands of people were walking around with portable, satellite-tracked computers that could load third-party applications. It was a technological development that made Uber’s vertical innovation possible.

Suddenly, ride-hailing was cashless, because payments could be handled through mobile. It was more reliable, because drivers found it harder to deny rides based on the destination. And because hailing and pick-up were both handled on a smartphone, it was accessible: you could get a ride almost anywhere at almost anytime, just by pressing a button.

Takeaways

The ride-hailing industry that Uber wanted to take on was rife with the kind of fierce competition that Thiel dislikes.

But Uber didn’t try to compete directly with the cab companies. Instead, Uber rose above the competition and built itself a monopoly (however short-lived) with a solution to one of the biggest problems in the ride-hailing industry: the difficulty of actually getting a ride.

With surge-pricing, Uber found a way to fix a key problem in taxi industry — equalizing supply with demand. When demand outpaces supply on rainy days or New Year’s Eve, the fare goes up, incentivizing more drivers to get out on the road. On slower days, when supply outpaces demand, the fare goes down, reducing driver idle time. Co-founder and former CEO Travis Kalanick once said, “We are not setting the price. The market is setting the price.”

Uber, however, didn’t go to an established market with this innovation. It didn’t become a cab-order service by recruiting taxi and limo drivers. It generated its own supply — independent drivers looking for extra income — and created a new market. Uber did exactly what Thiel argued innovators should do: avoid established markets because competition kills profit.

Yet, even “0 to 1” innovators like Uber can’t hold back competitors indefinitely.

In 2016, Uber sold its Chinese subsidiary to DiDi Chuxing after an intense price war ate away at its margins. DiDi’s victory in the Chinese market suggests an uncomfortable truth — imitative, “1 to n” thinking can also be a powerful engine of growth.

5. Customer Experience Innovation: Jeff Bezos

Many businesses have distinguished themselves by taking a customer-centric approach. Trader Joe’s set itself apart in the grocery market by emphasising its unique store experience. Home Depot has invested heavily in creating a more seamless online-to-retail experience than some other big-box retailers.

At Amazon, Jeff Bezos’s obsession with customers has been core to the company’s strategy from the beginning. It helped Amazon build out its core e-commerce business, and it has driven innovations such as its massive fulfilment network and Prime shipping. But it also guided its expansion into even more lucrative areas of business. Amazon Web Services, its cloud service, now accounts for most of its operating profit.

According to Bezos, “customers are always beautifully, wonderfully dissatisfied.” This simple insight is written into Amazon’s DNA — it guides product development processes, meeting structures, and back-end code. And it fuels Amazon’s relentless innovation in retail, software, grocery stores, healthcare, and finance.

How customer obsession gave rise to Prime

In the early years of e-commerce, Jeff Bezos recognised online shopping had to become more frictionless if it was going to be adopted by the masses. Optimising Amazon’s warehouse facilities to provide faster shipping and enabling one-click ordering had made a difference, but he intuited that there was still strong, implicit demand for even faster delivery of online goods.

“I remember him saying at the time that nobody wakes up every day hoping that their shipping would be just a little bit slower,” VP of AWS Dorothy Nicholls said.

Then came the idea for Amazon Prime: unlimited two-day-shipping anywhere in the contiguous US for an annual price of $79.

The idea was controversial internally: some thought that letting customers get automatic two-day shipping would bankrupt the company. Bezos himself wasn’t sure it wouldn’t.

The main problem was that expedited shipping was expensive. Executives feared that customers would love the program too much, take advantage of it, and run the company out of business.

Staying true to Bezos’s customer-centric vision, the team pushed through and launched Prime in 2005. Today, there are more than 100M Prime members in the US, and they reportedly spend on average $800 more annually than non-members.

Takeaways

The reason that the Amazon Prime experiment ultimately succeeded had nothing to do with complex math or spreadsheets. Shipping was expensive, and sending a toothbrush through the mail for delivery in two days was never going to be profitable for Amazon — especially not when the need for speed meant sending so many items through the air.

When one of Bezos’ lieutenants in operations pointed this out to him, he said, “You aren’t thinking correctly.”

“If customers liked Prime, the demand would go up,” Bezos said, and when demand went up, Amazon would have the “freedom to build new fulfilment centres.” It might be expensive to run Prime now, Bezos was saying, but the more people the company got to sign up for it, the cheaper it would get.

This basic flywheel can be used to understand how Amazon’s business works at the broadest level.

The more Amazon grows, the lower it can bring its cost structure and its prices, creating a better customer experience.

The better the Amazon customer experience, the more traffic it gets to the site, the more sellers it attracts to the platform, and the better the selection of goods it can offer. That leads to growth — but also to better customer experience.

Growth begets growth. But a flywheel like this takes effort and investment. Companies need to properly identify their customers’ problems and relentlessly work towards solving them. But once a flywheel like this gains momentum, it becomes a powerful engine of growth — one that can turn a small online bookstore into a global e-commerce powerhouse.

6. Customer Behaviour Innovation: Stewart Butterfield

To Stewart Butterfield, co-founder of Slack and before this, co-founder of Flickr, innovation isn’t the product itself. It’s the change in human behaviour.

Truly innovative products trigger a wave of change in how people do things. Facebook and Twitter, for example, changed how people keep in touch, share opinions, and stay up to date with the outside world. Spotify changed how people discover and listen to music. Waze, a crowdsourced navigation app, changed the way people drive.

But for Butterfield, building a good product alone can’t bring about that kind of broader change. To convince people to change their behaviour, you need to tell the right kind of story about your brand.

How Slack became the product that changed work

Slack branded itself as the product that would transform work. Teams that adopted Slack were going to save on communication costs, improve decision-making, and experience less stress.

The strength of the branding came from the fact that the team believed in the idea. In what is now one of the most famous internal business memos, Butterfield rallies his team by saying “what we’re selling is organisational transformation. The software just happens to be the part we’re able to build and ship.”

The media bought this narrative, Slack was “the email killer.”

Articles talked about how Slack would solve the problem of overflowing inboxes, buggy chat apps, and distracting colleagues. Slack was going to improve the lives of its users. The product’s launch page read “Be less busy” against a warm background image of a person leaning back with feet propped up on the desk.

Slack put out a powerful brand promise and looked to deliver on it by creating a thoughtful, well-designed product (working with MetaLab).

It worked closely with beta-testers to purposefully build out features that people would need and use. Given that Slack’s original team was a group of game developers, its designers were well-suited to making the product fun, learnable, and sticky. Once user groups hit 2000 messages, Slack found that there was a 93% chance that they would stick around for the long-run.

By hitting the sweet spot between branding and product development, Slack grew quickly. It became one of the fastest-growing enterprise products in history, with daily active users growing from 16,000 in 2014 to over 12M by late 2019.

It is now, during this COVID-19 scenario, becoming a ‘business critical’ application and experience for a very large number of businesses globally, and also this will carry into the future, which means that Stewart and the team will continue to change how people work together and how work gets done.

Takeaways

Slack was hardly groundbreaking technology. Bundling team chat and file-sharing was something that competitors like Hipchat and Campfire were already doing.

However, most users didn’t recognise that team collaboration tools made up a software category. During Slack’s beta period, Butterfield says, “When we asked [most users] what they were using for internal communication, they said, ‘Nothing.’ But obviously, they were using something. They just weren’t thinking of this as a category of software.”

Slack saw an opportunity where its competitors didn’t, providing a chance to make Slack the category-defining product. It leveraged that opportunity by marketing a compelling angle.

Lyft is another company that marketed a change in human behaviour. Through branding efforts and in-app features, Lyft pushed the concept that ride-hailing can be pleasant and personable.

While Uber pioneered ride-hailing technology, it only offered a luxury black car service in the first few years of its launch. It was only when Lyft started its ride-hailing service that Uber launched UberX, allowing drivers to use their own cars for the first time.

Uber maintained an image of sleek detached professionalism, but Lyft went in the complete opposite direction. With a bubbly logo, bright pink colouring, and a fuzzy moustache as a mascot, it created an image of a friendly, easy-going brand.

When a series of scandals disrupted Uber’s business, Lyft bolstered its friendly brand identity. It ran ad campaigns with the message, “It matters how you get there” and instituted driver-friendly features such as default tipping.

A Lyft ride was meant to feel less like a transaction and more like hitching a ride in a friend’s car. The relationship between the driver and the rider was pitched as being more equal, and the interaction more human. This touted perception of ride-hailing, aimed at changing consumer behaviour, helped Lyft to cut away at Uber’s market lead and grow twice as fast in the run-up to their public offerings last year.

7. Cultural Innovation: Ed Catmull

Ed Catmull, co-founder and former president of Pixar, doesn’t think that innovations come from good ideas. It comes from talented people — like Pixar’s hundreds of animators and producers — collaborating to make something greater than the sum of its parts.

To Catmull, the blueprint of an innovative organisation is a strong culture rooted in open and honest communication. The stage for innovation is set when creatives from diverse backgrounds feel empowered to share ideas that aren’t fully developed and give each other compassionate, constructive feedback.

Without a culture of honesty, people shy away from asking for help or sharing bold, risky proposals. Such an approach can lead to missed deadlines, mediocre products, and inconsistent quality.

People at Pixar think that great stories begin with an “ugly baby” — a seemingly bad idea. Yet, the studio has produced blockbuster after blockbuster, from “Toy Story” to “Coco,” that outperform their budgets by creating an environment in which all kinds of ideas are shared and nurtured.

How Pixar built a culture of creativity

Pixar’s iconic culture, to which Catmull attributes the company’s ongoing success, began to take shape during the production of “Toy Story,” its first feature-length animation.

The “Toy Story” directors and producers had a unique working relationship. According to Catmull, “Since they trusted one another, they could have very intense and heated discussions; they always knew that the passion was about the story and wasn’t personal.”

That gave rise to Pixar’s brain trust — a peer-driven feedback system for directors.

At any point, directors can present whatever they have to a group of other directors, producers, and writers — like-minded creatives — and get honest feedback on how their projects are going.

In addition to the brain trust model, Pixar uses the practice of dailies to encourage continuous feedback and build trust between team members. Animators review their progress with the director at the end of each day, setting aside any fear about presenting unfinished work.

These ideas helped Pixar figure out the crucial second act of “Toy Story 3,” which earned over $1B. It helped the director of “Inside Out” gain confidence in his vision — telling a story from the point of view of emotions living inside the mind. And it also helped reshape the ending of “Wall-E,” a movie which ended up making almost 3x its production budget.

Takeaways

Few film studios have achieved anything resembling the amount of success that Pixar achieved under Catmull. Since 1995, Pixar has put out over 20 feature films that have grossed a combined total of more than $14B and garnered almost 40 Academy Awards.

The key to that success has been Pixar’s ability to attract and retain the best people — not purely design skills, or storytelling ability, or any other kind of secret sauce.

The initial production on “Toy Story 2,” according to Catmull himself, did not go well. The leaders from the first “Toy Story” were busy on another movie, and so the project was taken up by another team at Pixar. It wasn’t until John Lasseter, Joe Ranft, Andrew Stanton, and Lee Unkrich rejoined the production that the film got back on track.

“It taught us an important lesson about the primacy of people over ideas,” Catmull writes of the incident, “If you give a good idea to a mediocre team, they will screw it up; if you give a mediocre idea to a great team, they will either fix it or throw it away and come up with something that works.”

The standard Hollywood studio doesn’t think in terms of “teams” this way. Instead, as Fast Company co-founder Bill Taylor writes for the Harvard Business Review, what you get in the traditional Hollywood model is that “highly talented people agree to terms, do their jobs, and move on to the next project.” It’s essentially a mercenary approach.

At Pixar, on the other hand, you have “a tight-knit company of long-term collaborators who stick together, learn from one another, and strive to improve with every production.” Everything from the creative freedom of the brain trust to Pixar University — which offers employees access to classes on everything from fine art to illustration — is designed to promote this kind of retention.

The result is that when Pixar writers or directors have hits, they don’t go looking for a payday from another studio — they strap in and get ready for their next Pixar film.

Overall Takeaways

So, the question I ask you to think on ….how do you combine the flavours to create an innovation framework which fits best for your businesses culture, operating model, ambition and risk appetite?

They are not all created equal, they all are hard to enable and sustain if the whole business is not aligned to the right approach and finally …this is an innovation journey, so you will need to mix flavours, not pick one and stick with it.